Canada-China Trade: 2021 Year in Review

Darren Choi - 22 March 2022

Canada-China trade grew steadily over 2021. Canadian exports to China grew at the highest rate seen since 2018 and growth in Canadian imports from China was the highest it has been in over a decade.

Growth in Canada-China trade has defied pandemic trends in the past couple years. Year-over-year, Canada-China trade growth was outpaced by Canada’s total trade growth with the world in 2021. However, growth in Canadian trade with other countries is mostly attributable to a post-pandemic bounce back in global trade. In contrast, Canada-China trade in 2021 continues the pattern of steady growth seen even during the height of the pandemic in 2020. When comparing levels of trade in 2021 with pre-pandemic levels in 2019, the steady growth in Canada-China trade (in both exports and imports) is striking.

The following data is gathered from Statistics Canada for goods (merchandise) trade with China, presented on an unadjusted customs basis in Canadian dollars (CAD). The relevant HS 6-digit identification code is used to identify individual products.

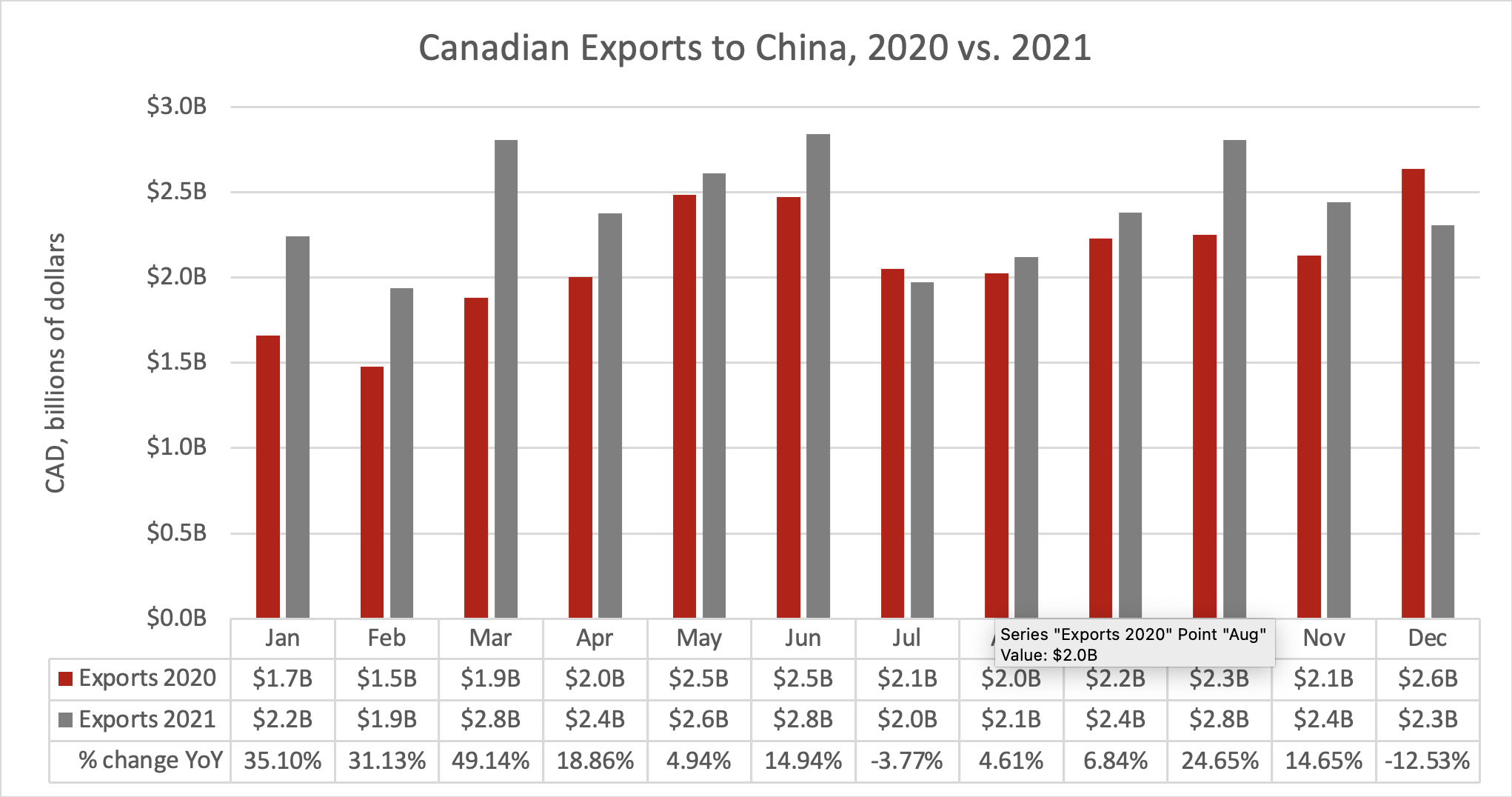

Canada-China Trade: 2021 YTD

Source: Trade Data Online (Statistics Canada – Customs Data)

Canadian exports to China grew 14% year-over-year in 2021, the largest growth rate seen since 2018 (when Canadian exports to China grew by +17.29% YoY). Moreover, the total value of Canadian exports to China surpassed the previous record set in 2018 (when Canada exported $27.69 billion worth of goods to China).

On the surface, it seems that year-over-year growth in Canadian exports to China underperformed relative to the overall growth rate in Canadian exports, which jumped a historic 20.67% year-over-year in 2021. However, this dramatic growth in overall Canadian exports is a clear product of the post-pandemic rebound in global trade. The difference between total Canadian exports in 2019 and 2021 (i.e. pre- and post-pandemic) is a more modest 6.55%.

Canadian exports to China, on the other hand, grew in 2020 even during the height of the pandemic. 2021 saw this steady growth continue. The robustness of this growth both during and after the pandemic is also evident in the 23.85% leap between total Canadian exports to China in 2019 and 2021.

Both October and November 2021 recorded strong export growth compared to the same month in 2020 (+24.65% and +14.65% YoY, respectively). However, December 2021 saw a sharp drop compared to December 2020 (-12.53% YoY).

Canadian exports of bituminous coal soared in 2021, vaulting it to first place among Canadian exports to China ($3.50 billion, +379.18% YoY). The significance of these coal export numbers is expanded upon in the Trends and Topics. Iron ore ($2.38 billion, -7.29% YoY), copper ore ($2.17 billion, +109.85% YoY), chemical wood pulp ($2.04 billion, +20.38% YoY), and canola seeds ($1.75 billion, +21.11% YoY) comprise the remaining top five export categories to China in 2021.

Canadian imports from China posted 11.96% year-over-year growth in 2021, the highest year-over-year growth seen since 2010 (when Canadian imports from China grew +12.26% YoY).

Year-over-year growth in overall Canadian imports slightly outpaced growth in Canadian imports from China in 2021. Once again, these numbers seem to be a product of the post-pandemic bounce back in global trade. The difference between overall Canadian imports in 2019 and 2021 is only 1.77%. Comparatively, Canadian imports from China posted a 14.19% rise from 2019 to 2021.

There was modest year-over-year growth in Canadian imports from China in October and November 2021 (+5.19% and +2.36% YoY, respectively). December 2021 saw a significant jump, however, at +16.54% YoY.

Consumer electronics made up four of the top five Canadian import categories from China in 2021. Laptops ($6.33 billion, +2.02% YoY) led the pack, followed by cell phones ($6.15 billion, +21.86% YoY) and network devices such as modems and routers ($2.41 billion, +12.16% YoY). Children’s toys, puzzles, and models ($1.36 billion, +9.38% YoY) were the only non-consumer electronics category in the top five, at fourth. Finally, video game consoles ($880.6 million, +17.8% YoY) was the fifth largest import category in 2021. The importance of consumer electronics to the Canada-China trade relationship is notable given the continued and acute shortages of electronic components and supply chain challenges in the electronic industry. We will explore supply chain issues in more depth in Trends & Topics.

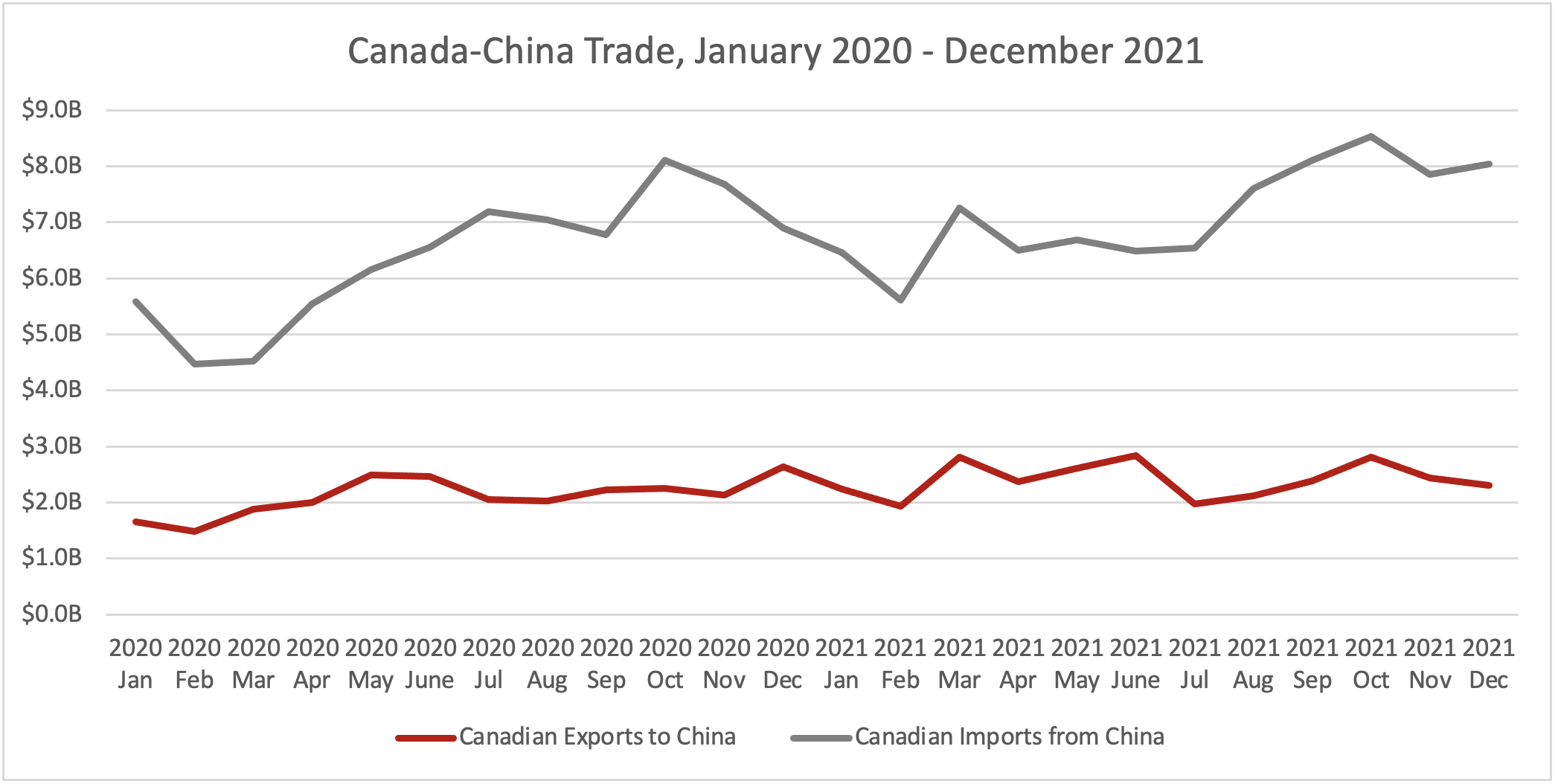

Canada-China Trade: Last 24 months (January 2020 – December 2021)

Source: Trade Data Online (Statistics Canada – Customs Data)

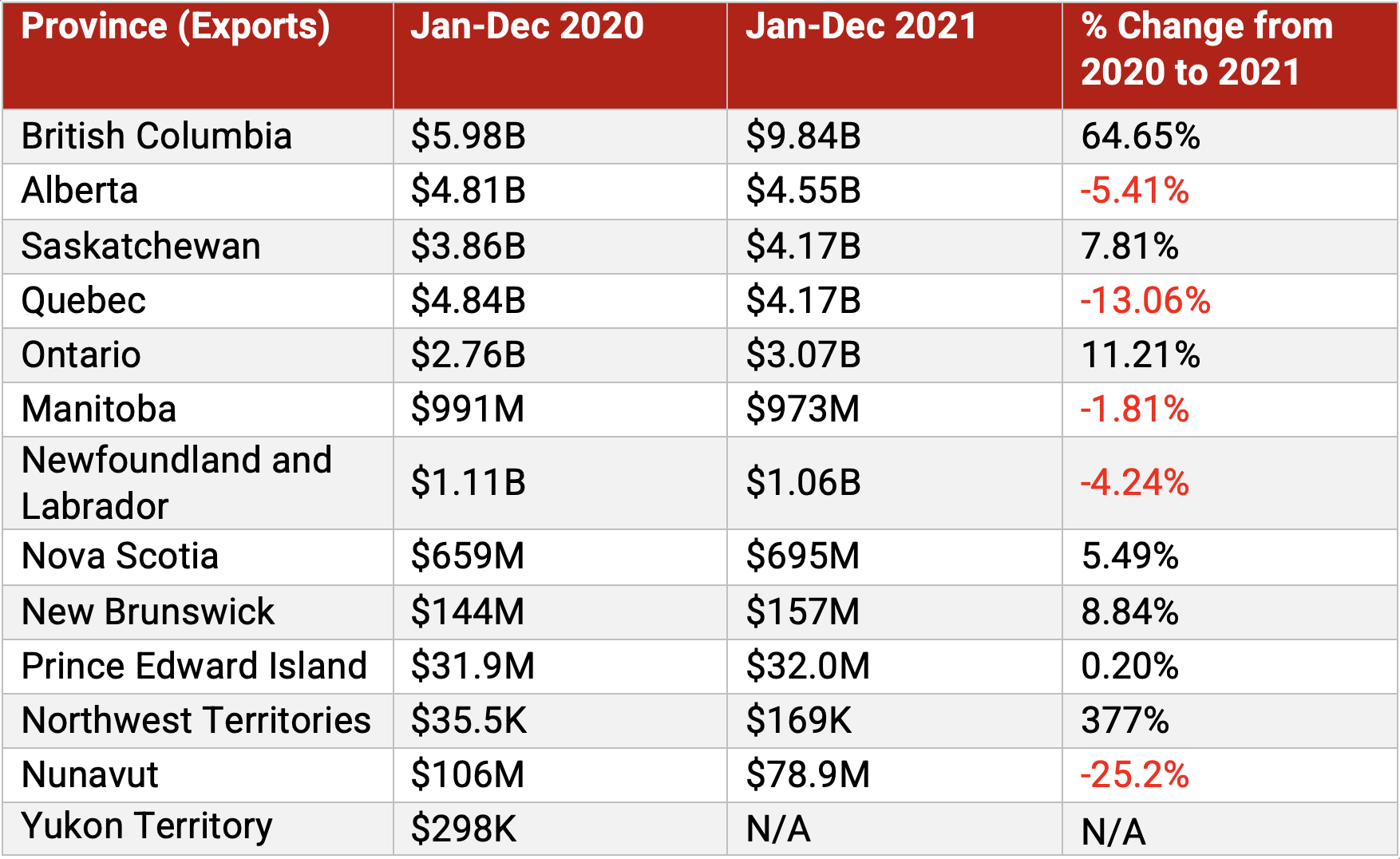

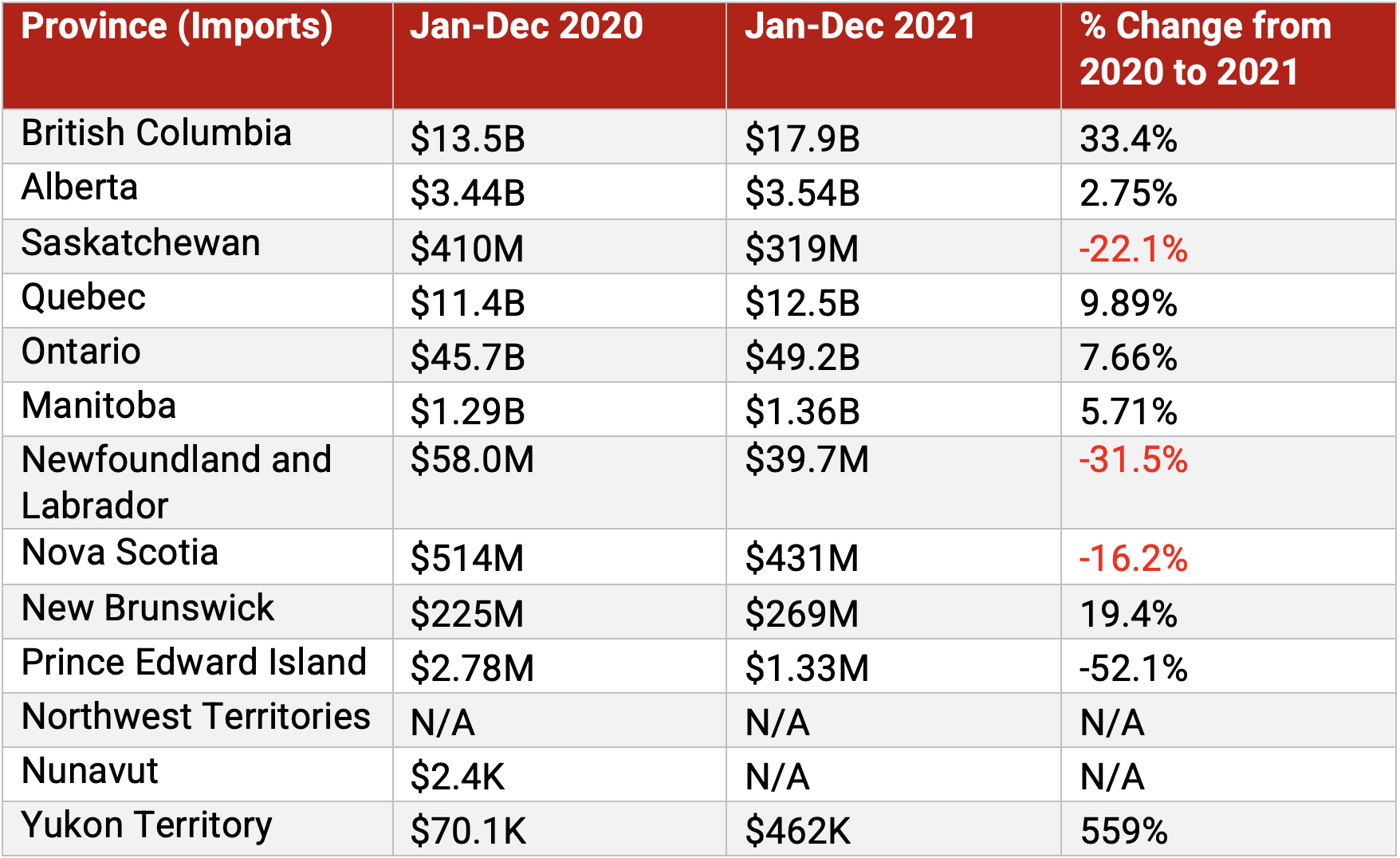

2020 vs. 2021 Canada-China Trade: By Province/Territory

Source: Trade Data Online (Statistics Canada – Customs Data)

Trends & Topics in Canada/China Trade

China’s Persistence in “Zero-Covid” Deepens Global Supply Chain Woes

COVID-19 has created major challenges for global supply chains: business and factory closures, supply and demand shocks, disruptions to mass transportation and shipping networks, etc. These challenges pushed an already-strained global supply chain well past its breaking point.

Importantly, China has been centre stage for many of these disruptions. Despite mounting competition, China retains its position as the “world’s factory.” China continues to be a hub for global manufacturing (accounting for some 29% of global manufacturing), is a significant source for raw and processed materials, and is a key player in global logistics and supply chains. Our trade reports certainly demonstrate this point when considering Canadian trade. The course of the pandemic and pandemic polices in China, now and moving forward, carry significant implications for the recovery and normalization of global supply chains.

Even before the pandemic, China’s end of the global supply chain was under strain. The US-China trade war created shocks challenged trans-Pacific business; the pandemic compounded by creating unprecedented disruptions to global supply chains.

The disruptions to global supply chains during the first weeks and months of the pandemic are familiar. COVID-19 outbreaks and subsequent lockdowns forced the shutdowns of factories and other industries. Global transportation and shipping networks were heavily disrupted; soaring shipping prices and shortages of containers were felt particularly acutely in China. Disruptions in China’s manufacturing and transport capacities led to shortages worldwide and bottlenecks in several key industries. Furthermore, these initial supply shocks early in the pandemic were followed by demand shocks later on; as restrictions lifted, businesses struggled to meet a sudden surge in consumer demand.

The pandemic is still ongoing, and it continues to disrupt aspects of the supply chain worldwide. Nonetheless, as pandemic restrictions subside, many expect supply chains to begin normalizing. However, many observers note continuing challenges in restoring supply chains to their pre-pandemic capacities that are directly linked to the current course of Chinese pandemic policy.

Unlike most of the world, China persists in a “dynamic zero-COVID” strategy. China is nearly alone in continuing to use strict lockdowns and restrictions on movement to prevent and contain any possible spread of COVID-19. Observers worldwide worry this strategy is prolonging supply chain disruptions and intensifying worldwide inflation. Continued harsh lockdowns disrupt manufacturing and further constrain China’s ability to supply key products, components and materials. China’s harsh restrictions on movement complicate the transportation of goods, often stranding them for extended periods of time. Furthermore, the transmissibility of the Omicron variant evades even China’s strict lockdowns, pushing Chinese policymakers to impose wider and stricter lockdowns throughout China during Q4 2021 and Q1 2022.

China stands increasingly alone in its “dynamic zero-Covid” pandemic approach. However, as the “world’s factory,” global supply chains are partially hinged on Chinese pandemic policy. Until China moves away from massive lockdowns and other hard measures that lead to disruptions to manufacturing, transportation, and shipping, global supply chains will likely not fully recover. For now, observers will watch China very closely for any sign of abandoning or modifying “dynamic zero-Covid.”

Canadian Coal Exports Surge Amidst China’s Energy Crunch

China faced a historic energy crisis in 2021. Energy demand soared, while the energy supply faced unprecedented shortages. As a result, Chinese energy prices hit record highs. Resurgent global demand for Chinese goods, extreme weather, a stronger push for green energy, and thermal coal shortages are among the many contributing factors to China’s energy crunch. In response, some provinces imposed strict power rationing, while the Chinese government made significant effort to expand the power supply. Importantly, these efforts were dependent on fossil fuels, particularly coal.

Thus, China, already the world’s largest coal consumer, saw a significant increase in its demand for coal. Asian coal prices surged as domestic Chinese coal sources could not meet this demand. Moreover, Australian coal continues to be banned in China. In this vacuum, Canada is clearly among the many coal-exporting countries that filled this gap. While bituminous coal exports are not necessarily the only thermal coal, it is certainly a significant percentage of Canadian coal exports. With 2021 concluded, we can fully discern the scale of this surge in Canadian exports of bituminous coal to China.

In 2020, total Canadian exports of bituminous coal decreased significantly, falling -35.68% year-over-year. However, in 2021, Canadian bituminous coal exports jumped 66.26% to $7.56 billion, above 2019 levels. This was almost entirely driven by a surge in Canadian exports of coal to China. Exports of bituminous coal to other nations grew only 6.35%. In contrast, Canadian exports of bituminous coal to China surged 379.18% to $3.50 billion, accounting for 46.33% of total Canadian exports of bituminous coal in 2021. China surpassed Japan to become Canada’s leading destination for bituminous coal exports in 2021.

A unique set of pressures force China to import large amounts of foreign coal in 2021. In the long-term, such levels of coal exports to China are likely unsustainable. China continues to pursue its climate goals and expand its renewable energy capacity. Simultaneously, China looks to cut coal imports through a massive boom in domestic coal mining. Conversely, Canada pledged at COP26 to end all thermal coal exports by 2030.

Policy pressures from both sides of the Pacific likely means 2021 was a flash in the pan for Canadian coal exports to China.

The Canada-China relationship: “Major issue” resolved, trade continues, but public opinion damaged

Canada-China relations were under a microscope in 2021 as political tensions continued to be at the forefront of Canada’s public discourse on China. The issue of Meng and the Michaels has dominated Canada-China relations since late 2018; the simultaneous releases and return of Meng and the Michaels to their respective nations is without doubt the most important development in Canada-China relations of 2021. Resolving what former Ambassador Barton called the “major issue” in Canada-China relations could be an opportunity for rapprochement; however, the wider damage to Canada-China relations may linger for some time.

With respect to trade, the ups and downs of the Canada-China political relationship have had less effect than some feared. These trade reports find that Canada-China trade has continued mostly unabated throughout the saga of Meng and the Michaels, the US-China trade war, and COVID-19. Some specific trade issues such China’s ban on Canadian canola seeds may benefit from better relations. Overall, however, Canadian trade with China has proved remarkably resilient when faced with political tensions and a global pandemic. This at least in part can be attributed to the complementary nature of the two economies.

Less directly, however, political tensions (including but not limited to Meng and the Michaels) have soured many in the Canadian public towards Canada-China trade. An Angus Reid poll conducted in November 2021 indicated 61% of Canadians would prefer if Canada reduced its trade relationship with China. Simultaneously, however, the poll showed that 58% of Canadians are worried about the economic consequences of standing up to China.

This poll is one of many indicating the Canadian public’s growing unease with engagement with China. We have not yet seen these sentiments affect bilateral trade. Even if public opinion were to sour further, it is not clear how that would impact different aspects of Canada-China relations.

Going into 2022, policymakers and Canadian public will be largely occupied by Russia’s invasion of Ukraine. On one hand, less scrutiny could provide an opportunity for Canada-China relations to improve and the development of further economic cooperation. On the other, however, Canadians might also reconsider our relationships with authoritarian nations in general. We will see whether Canada-China trade will remain resilient in the face of political strife and public opinion. Further disruptions to global trade and supply chains linked to the war in Ukraine is another roadblock to Canada-China trade relations throughout 2022.

Author

Darren Choi

Policy Research Assistant

Darren Choi is a Policy Research Assistant at the China Institute at the University of Alberta and a BA graduate with a major in Political Science and a minor in history.